The Definitive Guide to Crafting a Robust Business Partnership Agreement

Why a Business Partnership Agreement is Non-Negotiable

Many entrepreneurs, driven by the excitement of a new venture, often overlook the necessity of a formal partnership agreement, believing that trust and shared goals are sufficient. This oversight is a significant risk. While trust is indeed the bedrock of any successful relationship, a business partnership agreement serves as a vital risk management tool, a roadmap for operational clarity, and a legally binding safeguard against unforeseen challenges.

Consider this: studies suggest that a significant percentage of business partnerships encounter disputes, with some estimates indicating that nearly 70% of partnerships face challenges that could lead to dissolution if not properly managed. The primary culprit? A lack of clear, documented expectations and resolution mechanisms. Without an agreement, partners are often left navigating complex scenarios with differing interpretations, leading to costly legal battles, emotional strain, and ultimately, the collapse of the business.

Beyond Trust: Legal Protection and Dispute Resolution

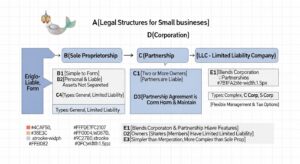

A partnership agreement transforms abstract expectations into concrete, enforceable terms. It defines the legal structure of your partnership, whether it’s a General Partnership (GP), Limited Partnership (LP), or Limited Liability Partnership (LLP), and outlines the specific rights and obligations of each partner under the law. This legal clarity is paramount. In the absence of an agreement, state laws often dictate how partnerships operate, which may not align with your specific intentions or desired outcomes.

Moreover, even the strongest bonds can fray under financial pressure or strategic disagreements. An agreement pre-emptively establishes a framework for dispute resolution – from informal negotiation to mediation or binding arbitration – saving countless hours and resources that would otherwise be spent in contentious litigation. It provides a structured path forward when conflicts arise, ensuring the business can continue to function while issues are addressed.

Mitigating Financial, Operational, and Reputational Risks

* Financial Risks: Who is responsible for debt? How are capital calls managed? What happens if one partner cannot meet their financial obligations? The agreement answers these questions, preventing financial burdens from unfairly falling on one partner.

* Operational Risks: Clear roles and responsibilities minimize operational bottlenecks and power struggles. It defines who makes day-to-day decisions, who has signing authority, and how major strategic choices are made.

* Reputational Risks: In cases of partner misconduct or legal issues, the agreement can outline how the partnership will respond, potentially protecting the reputation of the innocent partners and the business itself.

Setting Expectations: Roles, Responsibilities, and Contributions

One of the most common sources of conflict in partnerships stems from mismatched expectations regarding effort, contribution, and compensation. A robust agreement meticulously details:

* Specific Roles and Duties: What exactly is each partner expected to do? What are their areas of expertise and authority?

* Capital and Sweat Equity Contributions: Beyond initial financial investment, how are ongoing capital needs addressed? How is “sweat equity” (time, effort, intellectual property) valued and accounted for?

* Time Commitment: Is it a full-time endeavor for all partners, or are some passive investors? Clarity here prevents resentment and ensures equitable workload distribution.

By addressing these critical aspects upfront, a partnership agreement fosters transparency, accountability, and a shared understanding of the commitment required from each individual. It’s not just a legal document; it’s a foundational blueprint for a resilient and successful collaborative future.

The Foundational Elements: What Every Partnership Agreement Must Cover

A comprehensive business partnership agreement is a living document that anticipates and addresses a multitude of scenarios. While specific clauses will vary based on the nature of your business and partnership, certain foundational elements are universally critical. Overlooking any of these can leave significant vulnerabilities.

1. Partnership Name & Purpose

* Identification: Clearly state the legal name of the partnership and the names of all partners.

* Business Purpose: Define the primary business activities, objectives, and scope of the partnership. This prevents partners from unilaterally expanding the business into unrelated ventures.

* Location: Specify the principal place of business.

2. Term of Partnership

* Duration: Is the partnership for a fixed term (e.g., five years) or indefinite?

* Renewal/Termination: How will the partnership be renewed or terminated at the end of a fixed term? What are the conditions for early termination?

3. Capital Contributions

This is often a major point of contention if not clearly defined.

* Initial Contributions: Detail each partner’s initial contribution – cash, assets (e.g., equipment, real estate), intellectual property, or services (sweat equity). Specify the agreed-upon valuation for non-cash contributions.

* Future Contributions: Outline the process for requesting additional capital contributions from partners, including voting requirements, notice periods, and consequences for non-compliance (e.g., dilution of ownership, interest charges).

* Loans: Differentiate between capital contributions and loans made by partners to the partnership, specifying interest rates and repayment schedules.

4. Profit & Loss Distribution

Equitable distribution of profits and losses is crucial for partner harmony.

* Profit Sharing: How will net profits be distributed? Is it based on capital contributions, ownership percentage, effort, or a combination? Specify the frequency of distributions (e.g., quarterly, annually).

* Loss Allocation: How will business losses be absorbed by the partners? This is particularly important for general partnerships where personal liability is a factor.

5. Management & Decision-Making

Clarity here prevents power struggles and operational paralysis.

* Roles & Responsibilities: Clearly define each partner’s role, specific duties, and areas of authority.

* Decision-Making Authority:

* Day-to-day Operations: Who has authority for routine decisions?

* Major Decisions: What constitutes a “major decision” (e.g., capital expenditures over a certain amount, hiring/firing key personnel, strategic shifts, taking on significant debt)?

* Voting Rights: How are major decisions made? By unanimous consent, simple majority, supermajority, or based on ownership percentage?

* Meetings: Specify the frequency of partner meetings and record-keeping requirements.

6. Salaries & Draws

How will partners be compensated for their work?

* Guaranteed Payments: Are partners entitled to a regular salary or guaranteed payment for services rendered, regardless of profit?

* Draws: How and when can partners take draws against anticipated profits? What are the limits?

* Expense Reimbursement: Outline the process for partners to be reimbursed for business expenses.

7. Admission of New Partners

Planning for growth is essential.

* Process: Detail the procedure for admitting new partners, including voting requirements, capital contributions, and modification of the existing agreement.

* Conditions: Specify any conditions new partners must meet.

8. Withdrawal, Retirement, or Death of a Partner (Buy-Sell Provisions)

This is arguably one of the most critical and often overlooked sections. It dictates the future of the business if a partner leaves, becomes incapacitated, or passes away.

* Trigger Events: Define events that trigger buy-sell provisions (e.g., voluntary withdrawal, retirement, death, disability, divorce, bankruptcy, breach of agreement).

* Valuation Methodology: Crucially, specify how the departing partner’s interest will be valued. Common methods include:

* Book value

* Agreed-upon formula (e.g., multiple of earnings)

* Independent appraisal

* Periodic re-valuation

* Buy-Out Terms: Outline the terms of the buy-out, including payment schedule, interest rates, and security for the purchase price.

* Funding: How will the buy-out be funded? (e.g., cash reserves, installment payments, life insurance policies, disability insurance).

* Right of First Refusal: Give existing partners the right to purchase a departing partner’s share before it’s offered to external parties.

9. Dispute Resolution

A clear pathway to resolving conflicts saves time, money, and relationships.

* Hierarchy: Establish a tiered approach:

* Informal Negotiation: Partners attempt to resolve issues directly.

* Mediation: A neutral third party facilitates discussions.

* Arbitration: A neutral third party makes a binding decision.

* Litigation: As a last resort, in court.

* Costs: Who bears the costs of mediation or arbitration?

10. Dissolution of Partnership

Plan for the end from the beginning.

* Triggers: What events would lead to the dissolution of the partnership (e.g., mutual agreement, bankruptcy, inability to achieve purpose)?

* Process: Outline the step-by-step process for winding up the business, including asset liquidation, debt repayment, and distribution of remaining assets to partners.

* Liabilities: How are outstanding liabilities handled?

11. Confidentiality & Non-Compete Clauses

Protecting your business interests post-partnership.

* Confidentiality: Prohibit partners from disclosing proprietary information during and after the partnership.

* Non-Compete: Restrict departing partners from competing with the partnership for a specified period within a defined geographical area. These must be reasonable to be legally enforceable.

By meticulously addressing these foundational elements, you establish a clear, legally sound framework that protects all partners and provides a stable foundation for the business’s future.

Diving Deeper: Advanced Clauses and Strategic Considerations

While the foundational elements cover the essentials, truly robust partnership agreements anticipate more complex scenarios and strategic needs. Incorporating advanced clauses can provide an additional layer of protection, flexibility, and foresight for your business.

1. Intellectual Property (IP) Ownership

In today’s knowledge economy, intellectual property is often a business’s most valuable asset.

* Creation & Ownership: Clearly define who owns IP created by partners within the scope of the partnership (e.g., patents, copyrights, trademarks, software, trade secrets). Typically, IP created for the partnership is owned by the partnership.

* Pre-existing IP: Address any IP brought into the partnership by individual partners, clarifying licensing agreements or ownership transfers.

* Post-Partnership Rights: What rights do individual partners have to use IP after leaving the partnership?

2. Exit Strategies Beyond Dissolution

A partnership agreement isn’t just about how to break up; it’s also about how to evolve.

* Mergers & Acquisitions (M&A): How will the partnership respond to an offer for acquisition? What are the voting thresholds required for acceptance? How are proceeds distributed?

* Succession Planning: If the business is intended to continue beyond the current partners, outline a succession plan, especially for family businesses or long-term ventures.

* Tag-Along Rights: If a majority partner sells their stake, minority partners may have the right to sell their shares on the same terms.

* Drag-Along Rights: If a majority partner agrees to sell the company, they can compel minority partners to sell their shares as well, ensuring a smooth acquisition process.

3. Performance Metrics & Review

For partnerships where ongoing contributions vary, performance clauses can ensure accountability.

* Key Performance Indicators (KPIs): Define measurable metrics for partner performance or contribution (e.g., sales targets, project completion rates, client acquisition).

* Review Process: Establish a regular (e.g., annual) review process to assess partner performance against agreed-upon KPIs.

* Consequences: What happens if a partner consistently underperforms? This could range from reduced draws to mandatory buy-out provisions, though such clauses require careful legal drafting.

4. Indemnification Clauses

These clauses protect partners from financial liability arising from the actions of another partner or the partnership itself.

* Mutual Indemnification: Partners agree to indemnify each other against losses incurred due to the partnership’s activities, provided they acted in good faith.

* Specific Indemnities: Indemnification for specific risks or past liabilities known at the time of agreement.

5. Governing Law and Jurisdiction

This clause specifies which state’s laws will govern the interpretation and enforcement of the agreement.

* State Law: Crucially important for legal enforceability, especially if partners reside in different states or the business operates across jurisdictions.

* Jurisdiction: Designate the specific courts or tribunals where any legal disputes will be heard.

6. Force Majeure

A “Force Majeure” clause excuses partners from fulfilling contractual obligations due to unforeseen circumstances beyond their control.

* Defined Events: Specify events like natural disasters, acts of war, pandemics, or government actions that would trigger the clause.

* Impact: Outline the impact of such events on partner responsibilities and timelines.

7. Non-Solicitation

Similar to non-compete clauses, non-solicitation clauses prevent departing partners from poaching employees, clients, or suppliers from the partnership for a defined period after their exit. This protects the business’s relationships and human capital.

8. Valuation Methodology for Buy-Outs

While mentioned in foundational elements, deep diving into valuation methodology is a strategic consideration. Pre-agreeing on a detailed valuation method minimizes disputes during buy-outs.

* Formulaic Approach: Specify an exact formula (e.g., X times EBITDA, net asset value plus goodwill).

* Independent Appraisal: Agree on a process for selecting an independent appraiser and whether their valuation is binding.

* Periodic Review: Mandate regular (e.g., annual) updates to the business valuation or the valuation formula to reflect market changes and business growth.

By thoughtfully including these advanced clauses, you elevate your partnership agreement from a basic legal document to a sophisticated strategic tool that anticipates challenges, facilitates growth, and provides long-term stability for your business.

A Step-by-Step Framework for Drafting Your Agreement

Drafting a comprehensive business partnership agreement is a process that demands careful consideration, open communication, and professional expertise. Rushing this stage or relying solely on generic templates can lead to significant problems down the line. Here’s a step-by-step framework to guide you:

Step 1: Define Your Vision, Goals, and Expectations

Before you even look at a legal document, sit down with your prospective partners and have frank, in-depth discussions.

* Shared Vision: What is the ultimate goal of this partnership? Where do you see the business in 1, 5, 10 years?

* Individual Goals: What does each partner hope to achieve personally and professionally from this venture?

* Contributions: What specific skills, capital, networks, and time commitment will each partner bring? Be honest about strengths and weaknesses.

* Risk Tolerance: Discuss each partner’s comfort level with financial and operational risks.

* “What If” Scenarios: Brainstorm potential challenges – disagreements, underperformance, economic downturns, partner illness, or desire to exit. How would you ideally want to handle these?

This initial alignment is crucial. Any fundamental disagreements here should be resolved before proceeding.

Step 2: Open and Honest Communication

This step is an extension of Step 1 but focuses on laying everything out on the table. Create an environment where all partners feel comfortable expressing their expectations, concerns, and even their “deal breakers.” Discuss:

* Roles and Responsibilities: Who does what, and who reports to whom?

* Compensation and Distributions: How will partners be paid? What are the expectations for profit distribution?

* Decision-Making: Who has the final say on various types of decisions?

* Exit Scenarios: Discuss how a partner could leave, and how the business would continue.

Consider using a structured discussion guide or a facilitator if conversations become challenging. Documentation of these discussions, even informal notes, can be helpful later.

Step 3: Consult Legal Counsel (Non-Negotiable)

This is the most critical step. While online templates can provide a starting point, they are generic and cannot account for the unique nuances of your business, your specific state laws, or your partners’ individual circumstances.

Seek an Attorney: Engage a qualified business attorney specializing in partnership law. Ideally, each partner should have their own independent* legal counsel to review the agreement and ensure their individual interests are protected.

* Provide Information: Furnish your attorney with all the details from your Step 1 and 2 discussions. The more information they have, the better they can tailor the agreement.

* Understand Legal Implications: Your attorney will explain the legal implications of each clause and ensure the agreement is enforceable and aligns with current laws (e.g., SEC regulations if applicable, state partnership statutes).

Step 4: Draft the Agreement (Iterative Process)

Your attorney will typically prepare the initial draft based on your discussions.

Use a Template as a Starting Point (with Caution): For internal discussion before legal counsel, a template from reputable sources like LegalZoom or Rocket Lawyer can help you identify key sections. However, never* finalize or sign such a document without professional legal review and customization.

* Review Thoroughly: Read every clause, don’t skim. Ask questions about anything you don’t understand.

* Iterate: Expect multiple rounds of revisions. This is a negotiation, and it’s normal for partners to propose changes and clarify language.

Step 5: Review and Negotiate

Once the attorney drafts the document, each partner should:

Independent Review: Review the draft meticulously, ideally with their own independent* legal counsel. This ensures that no single partner’s interests are inadvertently or intentionally overlooked.

* Negotiate Terms: Come together to discuss any proposed changes or areas of disagreement. Approach this with a collaborative mindset, aiming for mutually beneficial solutions. Remember, the goal is a fair and balanced agreement that protects everyone.

* Document Revisions: Ensure all agreed-upon changes are accurately incorporated into the final draft by your attorney.

Step 6: Sign and Store

Once all partners and their respective counsels are satisfied with the final draft:

* Formal Signing: All partners must sign the agreement in the presence of witnesses, and ideally, a notary public (depending on state requirements and the nature of the partnership).

* Secure Storage: Keep original signed copies in a secure, accessible location (e.g., a bank safe deposit box, secure digital repository, or with your legal counsel). Provide each partner with a certified copy.

Step 7: Periodic Review and Updates

A business partnership agreement is not a set-it-and-forget-it document.

* Schedule Reviews: Plan to review the agreement at least annually, or biennially, even if no major changes have occurred.

* Trigger Events: Immediately review and update the agreement whenever there are significant changes to the business (e.g., new product lines, major investment, changes in market conditions, legal entity conversion) or to the partners’ circumstances (e.g., marriage, divorce, illness, desire to reduce involvement).

* Legal Counsel: Always involve legal counsel in any amendments or updates to ensure they remain legally sound and enforceable.

By following this structured framework, you significantly increase the likelihood of creating a robust, equitable, and effective partnership agreement that serves your business well for years to come.

Common Pitfalls to Avoid and Best Practices

Even with the best intentions, partnerships can falter if key errors are made during the agreement drafting process. Being aware of these common pitfalls and adopting best practices can significantly strengthen your partnership’s foundation.

Common Pitfalls to Avoid:

1. Relying on Trust Alone: This is the most prevalent and dangerous mistake. While trust is essential, it’s not a legal document. Business is dynamic, and circumstances change. A formal agreement protects the business and the partners when trust is tested.

2. Using Generic Templates Without Customization: Online templates are starting points, not final solutions. They rarely cover the unique aspects of your business, specific state laws, or the individual needs and contributions of your partners. “One-size-fits-all” rarely fits anyone perfectly.

3. Avoiding Difficult Conversations: Topics like exit strategies, disability, death, or underperformance can be uncomfortable to discuss. However, sidestepping these discussions upfront is a recipe for disaster later. A partnership agreement forces these conversations, and addressing them transparently builds a stronger foundation.

4. Not Involving Legal Counsel (or only one partner’s counsel): Attempting to draft an agreement without a qualified business attorney is a false economy. The cost of a poorly drafted agreement (or no agreement) in litigation, business dissolution, or lost opportunity far outweighs the legal fees. Furthermore, each partner should ideally have their own independent counsel to ensure their individual interests are represented.

5. Forgetting to Review and Update: Businesses evolve, and so should your agreement. An outdated agreement can become irrelevant, unenforceable, or even detrimental as your business grows or market conditions shift.

6. Lack of Clarity and Ambiguity: Vague language, undefined terms, or incomplete clauses create loopholes and opportunities for misinterpretation, leading to disputes. Every clause should be unambiguous.

Best Practices for a Resilient Partnership Agreement:

1. Transparency from Day One: Foster an environment of open and honest communication about expectations, contributions, fears, and aspirations. This sets a positive tone for the partnership.

2. Document Everything: From initial discussions to major decisions and financial transactions, maintain thorough records. This provides a clear audit trail and reference point.

3. Seek Professional Advice (Legal and Financial): Engage a qualified business attorney and, if necessary, a financial advisor or accountant. Their expertise is invaluable in structuring the agreement for legal enforceability and financial prudence.

4. Plan for the Worst, Hope for the Best: While optimistic, a robust agreement anticipates potential conflicts and challenges (e.g., partner death, disability, disagreement, underperformance, desire to exit) and outlines clear, fair mechanisms for addressing them. This is not a sign of distrust, but rather prudent risk management.

5. Focus on Clarity, Not Brevity: While conciseness is appreciated, do not sacrifice clarity for brevity. Ensure every clause is comprehensive, unambiguous, and covers all foreseeable scenarios. It’s better to have a slightly longer agreement that is clear than a short one that leaves critical gaps.

6. Implement a Valuation Methodology: Pre-agreeing on how the business (or a partner’s share) will be valued in various scenarios (buy-outs, dissolution) is a critical best practice that prevents significant disputes during exit events.

7. Regular Reviews: Schedule mandatory annual or biennial reviews of the agreement. This ensures it remains relevant, reflects the current state of the business, and accommodates any changes in partner circumstances or legal requirements.

By proactively avoiding these common pitfalls and diligently implementing these best practices, you can establish a strong, resilient foundation for your business partnership, minimizing future conflicts and maximizing your collective potential.

Conclusion: Build Your Future on a Solid Foundation

In the realm of business partnerships, a robust, well-crafted agreement is more than just a legal formality; it is the cornerstone of shared success and resilience. It serves as your partnership’s constitution, meticulously detailing the framework within which you will operate, grow, and navigate challenges. By clearly defining roles, responsibilities, contributions, and, crucially, exit strategies and dispute resolution mechanisms, you transform potential conflicts into manageable processes and vague expectations into actionable commitments.

This guide has underscored the imperative of moving beyond mere trust to establish a legally binding document that protects all partners and the